Is Hero Fincorp Share Price Set for Growth in 2025? Here's What You Need to Know

In today’s world, the financial sector plays an essential role in helping people and businesses meet their money needs. Many of us are familiar with banks, but there is another important group of financial institutions known as Non-Banking Financial Companies (NBFCs). NBFCs are organizations that offer many of the financial services that banks provide, such as loans and leases, but they do not operate like traditional banks. They do not accept deposits from the public in the same way, but they still help individuals, small businesses, and large companies get access to funds. This sector is especially vital in countries like India, where millions of people and businesses need credit but may not always have access to the strict banking channels.

NBFCs are innovative in their approach; they use creative methods to assess the creditworthiness of individuals who might not have a long history with traditional banks, helping to promote financial inclusion. This means that even if you do not have a strong credit history or all the usual paperwork, there may still be a way for you to access loans. In this article, we are going to take a very close look at one such NBFC, Hero FinCorp Limited, and explain everything in a beginner-friendly manner. We will break down what the company does, explain its key offerings, discuss the growth drivers that are fueling its expansion, and look at its financial health—all without assuming any prior financial knowledge.

Company Overview: Hero Fincorp Unlisted Shares

Registered with the Reserve Bank of India (RBI) and classified as an NBFC, the company focuses on providing finance and investment services. Unlike traditional banks, Hero FinCorp does not accept public deposits, which means that people do not simply deposit their money with them. Instead, the company raises funds from other sources and uses these funds to provide various types of loans and financial products.

Hero FinCorp’s business operations are centered on lending and leasing services. At its core, the company provides loans and advances, which means that they give money to customers with an agreement that the money will be paid back over time, usually with interest. They also offer leasing services, which is a way for businesses and individuals to use assets (like vehicles or equipment) without buying them outright. Leasing can be very useful for people who might not have the funds to purchase something immediately or who prefer the flexibility of renting instead of owning.

Loan Portfolio: Hero Fincorp Unlisted Shares

Hero FinCorp offers a wide variety of financial products, each designed to serve different customer needs. Let’s break down these offerings in simple, easy-to-understand language, using clear subtopics for each product category.

Vehicle Finance:

This service is mainly focused on providing loans for two-wheelers, which include motorcycles and scooters. Many people in India rely on two-wheelers for daily commuting, but often, they may not have enough money saved up to purchase one outright. Hero FinCorp steps in by offering loans specifically for two-wheelers. What makes their approach unique is that instead of relying solely on the conventional credit score, the company uses innovative methods to assess a customer’s creditworthiness. This means that when you apply for a two-wheeler loan, the company may also consider factors such as personal visits, local reputation, and background checks, which help them understand your ability to repay the loan better. Over the last financial year alone, Hero FinCorp disbursed more than one million two-wheeler loans.

Personal Finance:

Personal finance is another major area where Hero FinCorp makes a difference. Personal loans can be used for a variety of needs, such as paying for education, medical emergencies, home improvements, or even weddings. What is important here is that these loans are tailored to fit the needs of everyday people. They are offered through multiple channels, including in-house teams, call centers, and digital platforms. This ensures that no matter where a person lives or what their financial background is, they can get access to the funds they need.

Mortgage Loans:

Mortgage loans are provided by Hero FinCorp through its subsidiary, Hero Housing Finance. A mortgage loan is a type of loan that is used to buy a home or property. In simple terms, when you take out a mortgage, you borrow money to buy a house, and the house itself serves as collateral. This means that if someone is unable to repay the loan, the lender can take possession of the property. The company offers both residential and commercial mortgage loans. Residential mortgages are aimed at individuals and families looking to purchase or renovate a home, while commercial real estate lending is designed for businesses that need property for their operations, such as office buildings or retail spaces. In FY 24, the company had a direct exposure of over ₹1,700 crore in residential mortgages and more than ₹2,100 crore in commercial real estate lending. Additionally, the company also offers refinance facilities, which help customers manage their loans better by restructuring them.

MSME Finance:

MSME stands for Micro, Small, and Medium Enterprises. This segment is particularly important because it supports small businesses, which are the backbone of the economy. Many small business owners find it challenging to secure funds from traditional banks due to limited documentation or their smaller scale of operations. Hero FinCorp fills this gap by offering a range of financial products tailored to the unique needs of MSMEs. These products include supply chain finance, construction finance, business loans, and loans against property. The company operates from 74 locations, which means it has a strong physical presence and can process over 3,000 applications every month.

Corporate & Institutional Finance (CIF):

For larger companies and institutions, Hero FinCorp offers Corporate & Institutional Finance (CIF) services. These financial solutions are designed for businesses that require larger loans or specialized financial products. The CIF segment works alongside the MSME finance division, but it is tailored to meet the needs of bigger corporate clients. These clients often need more complex financial solutions, and the company uses a combination of its in-house sales teams and a network of Direct Sales Agents (DSAs) to reach out to and serve these customers. As of the end of the financial year 2023-24, the CIF segment had assets under management (AUM) of nearly ₹6,000 crore.

Beyond the core offerings, Hero FinCorp provides a bouquet of additional financial products that cater to various needs. These include used-car financing, which allows individuals to buy pre-owned vehicles; loyalty and open market personal loans, which may come with special benefits or rewards; partnership financing, which helps businesses collaborate and grow; unsecured business loans, where the borrower does not need to provide collateral; inventory funding, which is crucial for businesses that need to purchase stock; and supply chain financing, which helps companies manage the money flow in their operations. All these products are designed with the same goal in mind: to make financial services accessible to everyone, regardless of their credit history or traditional banking relationships. These offerings show the company’s flexibility and its willingness to innovate in order to meet the ever-changing needs of its diverse customer base.

Growth Drivers: Hero Fincorp

The impressive growth trajectory of Hero FinCorp can be attributed to several key drivers that have enabled the company to expand its market presence and enhance its financial performance. These growth drivers are interlinked, creating a strong foundation for both short-term gains and long-term sustainability.

Multi-Channel Distribution NetworkOne of the primary growth drivers for Hero FinCorp is its extensive multi-channel distribution network. The company reaches customers through various avenues such as in-house sales teams, call centers, digital platforms, and a vast network of Direct Sales Agents (DSAs). This diverse approach ensures that customers from different parts of the country and varying economic backgrounds have access to its financial products. By not relying on a single distribution channel, the company reduces its risk of market saturation in one area and instead benefits from a broad and balanced outreach strategy.

Strategic Treasury ManagementAnother important factor driving growth is the company’s focus on strategic treasury management. The treasury department is responsible for managing the funds that the company uses to lend money. This involves borrowing at competitive rates, maintaining sufficient liquidity, and investing surplus funds in safe, liquid instruments. Efficient treasury management ensures that the company always has the necessary resources to capitalize on new opportunities. This financial discipline not only supports day-to-day operations but also positions the company for future growth, thereby increasing investor confidence in the scope of Hero Fincorp unlisted shares.

Innovative Credit Assessment TechniquesHero FinCorp is well-known for its innovative approach to credit assessment. Traditional financial institutions often rely solely on numerical credit scores to evaluate borrowers, which can exclude many potential customers. In contrast, Hero FinCorp combines quantitative data with qualitative insights such as customer visits, local reputation, and background checks. This method allows the company to identify creditworthy individuals who might otherwise be overlooked. By tapping into an underserved market, the company not only fosters financial inclusion but also expands its customer base, which is a key driver of its growth.

Partnerships and Ecosystem IntegrationStrategic partnerships also play a crucial role in Hero FinCorp’s expansion. The company has established strong ties with partners like Hero MotoCorp, which enhances its vehicle finance segment by providing instant loan approvals through the integrated e-Fin marketplace. These partnerships create a seamless customer experience—from purchasing a vehicle to securing financing—thereby reinforcing the company’s reputation and market reach. Such collaborations also open up new avenues for cross-selling financial products, further boosting growth.

Scalability and Flexibility in OperationsAnother critical growth driver is the company’s ability to scale its operations while remaining flexible in its approach. Hero FinCorp’s systems are designed to handle a large volume of loan applications and adapt to changing market conditions. Whether it is through a new product launch or responding to regulatory changes, the company has built a resilient framework that supports continuous growth. This operational flexibility ensures that the company can seize emerging opportunities and mitigate risks effectively, thereby fostering sustained expansion.

Financial Standpoint FY 24: Hero Fincorp Unlisted Shares

The financial standpoint of Hero FinCorp is characterized by steady growth, strong profitability, and effective risk management. Understanding the company’s financial health is essential for both customers and investors, particularly those interested in the potential of Hero Fincorp unlisted shares.

Revenue Growth and ProfitabilityThe company's total income grew by 29%, from ₹6,033 crore in FY 2022-23 to ₹7,805 crore in FY 2023-24. The consolidated profit after tax increased from ₹479.95 crore to ₹637.05 crore during the same period, due to an increase in loan disbursements, diversified revenue streams, and effective management practices.

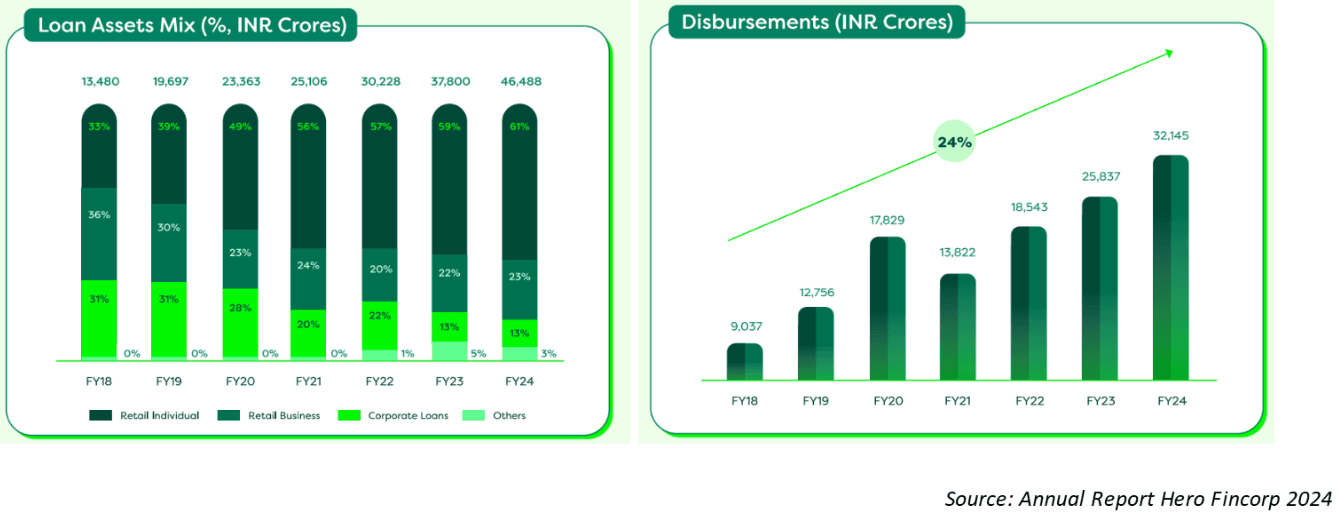

Asset Under Management (AUM) and Loan GrowthA critical measure of financial performance for lending institutions is the growth in assets under management (AUM). The company has experienced substantial growth in its AUM, which rose by 23% from ₹37,800 crore in FY 2022-23 to ₹46,488 crore in FY 2023-24. This growth in AUM, particularly in the retail segment, demonstrates effective deployment of capital and a corresponding increase in income-generating assets.

Cost Management and Funding EfficiencyWhile the company's finance costs are substantial, at ₹3,097.36 crore on a consolidated basis for 2023-24, the profit before finance costs, depreciation, and amortisation expenses also grew significantly, indicating effective cost management alongside business growth. The company sources funds through diverse methods such as secured and unsecured debentures, term loans, and commercial papers. This diversified funding strategy helps in keeping the borrowing costs at competitive rates, thereby improving overall profitability. In addition, effective cost management ensures that operational expenses do not outweigh the income generated, further bolstering the company’s financial stability.

Capital Adequacy and Financial StabilityThe company’s capital adequacy ratio (CAR) is a crucial indicator of its financial stability. A strong CAR indicates that the company has a sufficient buffer to absorb potential losses and continue operations without disruption. Hero FinCorp maintains a Capital Adequacy Ratio (CAR) of 16.28% as of March 31, 2024, well above the RBI's mandated norm of 15%. This strong capital position ensures that the company has adequate capital to manage its risks and support its operations, which ultimately contributes to profitability by providing stability and confidence to investors and creditors.

Risk Management Framework and Credit Quality

Hero FinCorp employs a risk management framework, which is designed to identify, prioritize, mitigate, monitor, and report threats to the company’s objectives, reputation, operations and compliance. The company uses a ‘Three Lines of Defence’ model and has a Risk Management Committee (RMC) that assists the Board. Key areas of focus include: Credit risk management, Fraud prevention, and Digitisation, automation, and cybersecurity. Hero FinCorp manages credit risk through structured processes, including credit appraisals and monitoring, and uses a Risk Appetite Framework to limit concentration risk.

A non-performing asset (NPA) is a loan for which principal or interest payments are overdue for a specific period. It's a key measure of a financial institution's credit quality.

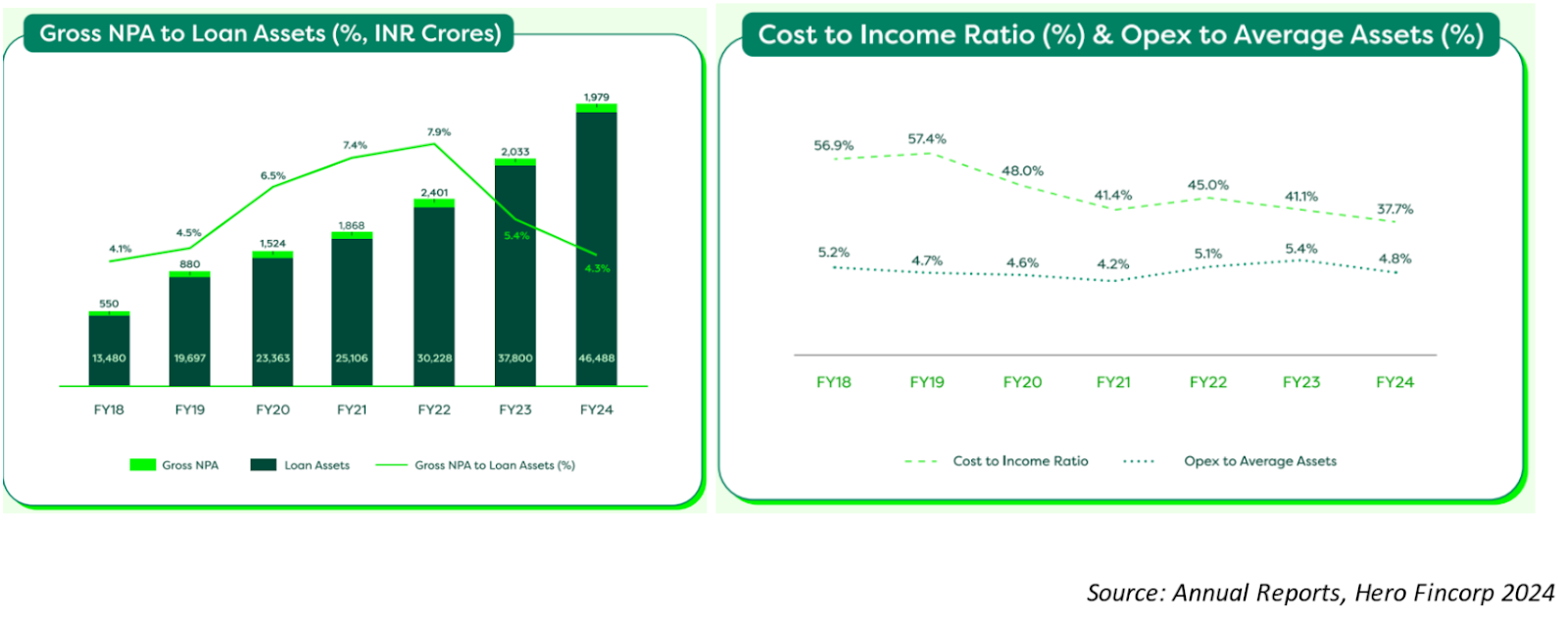

Gross NPA Trends: Hero FinCorp’s gross NPAs peaked at 7.9% in FY22, following the Covid-19 pandemic. The company reduced its gross NPAs to 5.38% in FY23 and further to 4.26% the next year. However, the gross NPA ratio had risen again to 5.36% by December 31, 2024.

Gross NPA to Assets Ratio: The gross NPA to assets ratio was 4.3% in the current financial year, down from 5.4% the previous year.

Cost-to-Income Ratio: The cost-to-income ratio for FY24 is 37.7%, a decrease from 41.1% in FY23, indicating that the company has improved its operational efficiency or reduced its expenses relative to income [sources not cited]. This suggests that the operating expenses have decreased as a percentage of total income

Latest: Jitters in the Quarterly Momentum- Q3 FY25

In Q3 FY25, while the overall performance remains strong in some respects, certain aspects of the quarterly results indicate volatility that appears to be influenced by broader macroeconomic conditions impacting the microfinance sector.

Revenue from Operations: For Q3 FY25, total revenue from operations increased by 15.3% YoY (Year-on-Year), reflecting continued growth in the loan book. On a QoQ (Quarter-on-Quarter) basis, total revenue grew marginally by 1.1%, with a 3.1% increase in interest income supporting this stability despite lower fee-based income from reduced other charges.

Expenses have risen sharply, increasing by 35.4% YoY due to the impairment on financial instruments, which surged by 62.2%, indicating a growing need for provisioning against bad loans. Finance costs also increased by 20.1% YoY, reflecting higher borrowing costs and a more challenging debt servicing environment.

Loan Write-offs: In the first three quarters of FY25, the company’s loan write-offs reached ₹2,180 crore, a substantial increase from the ₹1,214 crore in the same period the previous year. The company sold off over 2.95 lakh written-off loans worth ₹1,874.73 crore for just ₹49.85 crore.

Profitability: The net profit figures reinforce this downward trend. YoY, net profit declined from ₹200.43 crore in Q3 FY 24 to a net loss of ₹32.43 crore in Q3 FY 25 . QoQ, net profit dropped from ₹26.52 crore in Q2 FY 25 to a loss of ₹32.43 crore in Q3 FY 25 . These changes underscore the pressure on profitability, as rising costs and deteriorating asset quality erode margins.

Recent macroeconomic trends have had a pronounced effect on the microfinance (unsecured) sector, and these external pressures are reflected in the quarterly performance jitter observed for Hero FinCorp. Rising inflation, higher interest rates, and a slowing economic cycle have increased the stress on microfinance borrowers, who typically have limited financial buffers. Although these macro factors have introduced short-term volatility, they are part of a larger industry trend impacting many such companies. While the previous full-year performance was solid, the current environment has led to temporary setbacks that could be alleviated as macroeconomic conditions stabilize.

In conclusion, Hero FinCorp serves as a stellar example of how NBFCs can drive financial inclusion and growth through innovation and customer-centric practices. It is paving the way for a future where financial barriers are minimized, and opportunities for growth are maximized.