Fino Paytech: Analyzing Share Prices and Unlisted Shares for 2025

The world of financial services is undergoing a profound transformation, with technology playing a pivotal role in reshaping how people access banking, insurance, and credit. This shift, known as fintech, has introduced new opportunities for millions of people, especially those in underserved or rural areas where traditional banking infrastructure has often been inaccessible. Among the notable players in this fintech revolution is Fino PayTech, a company that is leveraging innovative technology to promote financial inclusion and make essential services accessible to everyone, regardless of location or economic status.

Looking ahead to 2025, Fino Paytech Share Prices will be underway, drawing significant attention from investors as the company continues to expand its footprint. With its broad range of services, including banking, insurance, micro-lending, and payments, Fino is well-positioned to play a major role in India's financial inclusion landscape. The evolving Fino Paytech share prices will likely reflect the company's growing influence, offering insight into how its innovative approach is transforming the financial services sector

Fino Paytech Share Price: Current Market Trends

With the government's strong push for digital inclusion and the growing demand for accessible financial services in rural India, Fino PayTech Unlisted Shares trading at [View Current Price of Fino Paytech] is well-positioned to capitalize on these evolving market dynamics. The company's focus on providing innovative financial solutions to underserved populations aligns perfectly with the current trends shaping the Indian fintech sector.

Increasing Adoption of Digital Financial Services

India’s shift towards digital finance has been one of the primary drivers for Fino PayTech. The government’s push for digital inclusion, through initiatives like Jan Dhan Yojana, Digital India, and the introduction of the Unified Payments Interface (UPI), has created a favorable environment for fintech companies like Fino. As more people in rural and underserved areas gain access to smartphones and the internet, there is a surge in demand for mobile-based financial services. This trend directly benefits Fino PayTech’s business model, which offers everything from basic banking services to micro-loans and digital payments.

Rural and Semi-Urban Market Penetration

One of Fino PayTech’s strongest growth drivers is its focus on rural and semi-urban markets. In these areas, access to formal banking infrastructure is often limited, creating an opportunity for fintech companies to step in and fill the gap. Fino’s micro ATM services, agent networks, and mobile banking solutions are crucial in making banking accessible to a large portion of the population that would otherwise be excluded from the formal financial system.

Adoption of Alternate Banking Models

As traditional banking channels become more saturated and less appealing to younger, tech-savvy populations, digital-first platforms like Fino are seeing rapid adoption. With services ranging from micro-lending to digital payments and mobile banking, Fino is positioned to capitalize on this shift toward non-traditional banking models. The increasing acceptance of mobile-first and internet-first banking solutions is a key trend that will continue to bolster Fino PayTech’s prospects in the market.

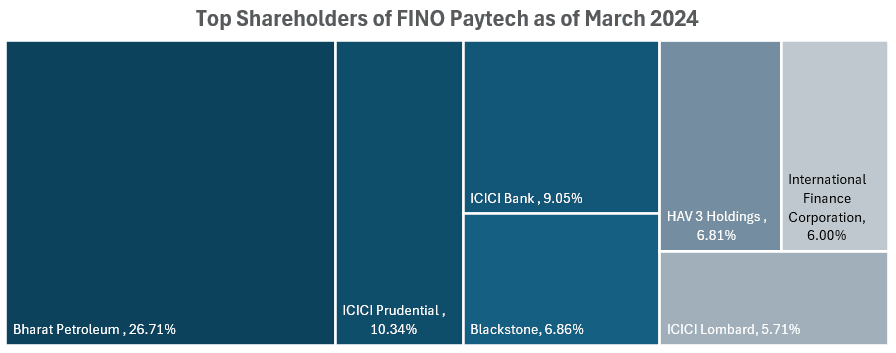

Unlike many traditional Indian firms, Fino PayTech has no promoter holding, indicating its independence from founder-driven control. Instead, its ownership structure features significant investments from global and domestic entities such as Bharat Petroleum Corporation (holding a 21.94% stake), ICICI, Blackstone, International Finance Corporation, etc.

This diverse investor base provides financial backing and strategic direction, positioning Fino PayTech as a robust player in the financial technology sector. The absence of a promoter-driven structure enables a governance model that balances investor influence with a focus on transparency and long-term value creation.

Who Are Its Clients?

Fino PayTech's client base is diverse, encompassing various sectors and institutions, which allows the company to have multiple revenue streams and reduces its reliance on any single sector. Here’s a more detailed look at their clientele:

- Banks: Fino PayTech provides its technology-driven solutions and services to banks. This includes offering a business and banking technology platform that integrates various financial services. The company also provides authentication services to banks which allows for secure verification of individuals, which is important for smooth banking transactions.

- Microfinance Institutions: Fino PayTech serves microfinance institutions, offering them technology-based platforms and services to enhance their operations. These services likely aid in the efficient delivery of microfinance solutions to underserved populations.

- Government and Non-Government Organisations: The company's clientele also includes both government and non-government organizations. This indicates that Fino PayTech's solutions are adaptable for use in various public and social sector initiatives.

- Insurance Companies: Fino PayTech provides its services to insurance companies, suggesting that they might offer technology for policy distribution or other related services. This highlights the flexibility of Fino PayTech's platform to support different types of financial products.

- Corporate Entities: Fino PayTech also works with corporate entities, further demonstrating the versatility of its technology platform. This may involve providing solutions that help streamline financial processes or improve access to financial services for corporate employees or partners.

- Business Correspondents (BCs): As part of its business model, Fino PayTech works with Business Correspondents, who are individuals or entities that act as intermediaries between banks (or financial institutions) and customers. They help extend banking services to areas where traditional bank branches or ATMs are not easily accessible. These BCs are a vital part of the service delivery channel, especially in reaching rural and underserved areas.

Fino PayTech’s operations revolve around three main components:

Business and Banking Technology Platform

The backbone of Fino PayTech’s operations is its comprehensive technology platform. This platform integrates a variety of financial services, such as customer account management, loan distribution, and transaction processing. By offering a unified system, Fino helps its clients operate more efficiently while reducing costs.

The platform also ensures scalability, enabling Fino to handle a growing number of transactions and users. This technological infrastructure allows the company to support diverse client needs, from basic banking services to advanced authentication solutions.

Service Delivery Channels

Fino PayTech ensures its services reach a wide audience through multiple delivery channels, including:

- Merchant Networks: Local merchants act as mini-banks, offering services like deposits, withdrawals, and bill payments.

- Micro ATMs: Portable devices that provide basic banking functions in rural areas.

- Digital Platforms: Apps and online services that cater to urban customers.

- Physical Branches: Traditional outlets for face-to-face banking services.

Revenue Streams

Fino PayTech earns revenue through:

- Sale of Goods: Selling prepaid cards, micro ATMs, and other devices.

- Service Fees: Commissions on transactions, enrollment income, and interest on loans.

- Core Banking Services (CBS): Providing technology solutions for banking operations.

Fino PayTech offers several unique services that set it apart from competitors. Let’s dive deeper into these offerings:

Authentication Services

Fino PayTech has established a strong presence in the identity verification space with UIDAI (Unique Identification Authority of India). This partnership allows Fino to offer secure Aadhaar-based authentication services that ensure high levels of trust and reliability in financial transactions.

For example, when the government needs to identify beneficiaries of social welfare schemes, Fino’s platform ensures accurate and fraud-free verification through Aadhaar-based authentication. This process plays a pivotal role in ensuring that financial services reach the right people, reducing the risk of fraud and making government schemes more effective.

Micro ATM Services

Micro ATMs represent a significant innovation for rural banking and financial inclusion in India. These portable, small-sized ATM devices enable banking services in remote locations where traditional ATMs or bank branches are unavailable. Micro ATMs allow users to perform basic banking operations such as:

- Cash withdrawals: Making it possible for people to access their funds without needing to travel long distances to a branch.

- Balance checks: Offering customers the ability to view their bank account balances on the spot.

- Payments: Facilitating utility bill payments, mobile recharges, and other essential transactions.

Lending Services

One of the standout features of Fino PayTech is its role in providing small loans to underserved individuals. Fino acts as a Business Correspondent (BC) for major banks and Non-Banking Financial Companies (NBFCs), facilitating the distribution of micro-loans. These loans are especially critical for low-income families, small businesses, and rural communities, as they provide the capital necessary to support entrepreneurship and personal growth.

By offering these loans, Fino ensures that communities that lack access to formal financial services can still receive credit. This model of direct loan distribution is particularly effective in rural areas, where traditional banking services might be scarce or non-existent. The micro-lending services enable individuals and small businesses to enhance their economic prospects, contributing to the growth of the local economy.

Retail Banking Services

Fino’s retail banking services form the backbone of its operations, making banking accessible to a large number of individuals through its expansive network of branches and merchants. These services include:

- Account openings: Enabling customers to open savings and other types of accounts through Fino’s outlets, offering basic banking services to those without access to formal banking channels.

- Money transfers and remittances: Providing an efficient way to transfer funds, whether it’s a small remittance sent home by migrant workers or larger sums for business transactions.

- Bill payments and recharges: Offering customers a one-stop solution to pay their utility bills and recharge mobile phones, an essential service in the digital age.

- Sales of financial products: Fino acts as an intermediary to sell products like insurance policies, offering customers easy access to financial tools they might not otherwise consider.

Financial Standpoint of Fino Paytech

Profitability: Fino PayTech, on a consolidated basis, reported a net profit of ₹80.83 crores in FY 2024, from ₹50.10 crores the previous year as a group. However, the parent company, Fino PayTech Limited, experienced a standalone loss of ₹7.24 crores during the same period, which was offset by the strong performance of its subsidiaries. This is primarily driven by the performance of Fino Payments Bank Limited. The overall profitability can also be attributed to several factors, such as a reduction in expenses and a lower provision for doubtful debts, which is the amount set aside for debts that may not be recovered. This amount has decreased from ₹33.12 crore to ₹3.05 crore. Additionally, the cost related to employee compensation linked to stock options nullified from ₹28.55 crore in the previous year.

Net Capital Turnover Ratio: This ratio has increased from 24% to 58%. This indicates that the company is becoming more efficient in using its working capital to generate revenue. This substantial increase could be driven by improved revenue and more efficient working capital management.

Trade Receivables Turnover Ratio: This ratio has increased from 2.2x to 4.1x. This implies that the company is collecting its receivables more quickly than the previous year, which is a positive indicator of cash flow management. This could also be a sign that the company is being more strict with its credit policy or recovering from the provisions taken in the previous year.

Investing in Fino Paytech Unlisted Shares: Opportunities and Considerations

Fino PayTech’s growth is fueled by several factors:

Focus on Financial Inclusion

India has millions of people without access to formal banking services. Fino’s mission to bridge this gap positions it well to tap into a large, underserved market. This focus aligns with national goals and attracts partnerships with both public and private entities.

Technology-Driven Solutions

By continuously upgrading its technology platform, Fino ensures its services remain efficient and scalable. For example, the integration of artificial intelligence and data analytics helps improve customer experience and operational efficiency. This technological edge keeps Fino competitive in the fast-evolving fintech sector.

Strong Subsidiary Performance

Fino Payments Bank Limited, a listed key subsidiary, reported impressive revenues of ₹1,478.38 crores and a net profit of ₹86.22 crores. This performance significantly boosts the group’s overall financial strength and underscores its potential for further growth.

Diverse Delivery Channels

Fino’s extensive service network, including merchant points, digital platforms, and micro ATMs, ensures its services reach even the most remote areas. This accessibility is a major driver of customer adoption.

Risks to Fino Paytech

Significant Credit Risk Exposure: Fino faces substantial credit risk, arising from its lending activities. The company has considerable amounts in trade receivables to Micro, Small, and Medium Enterprises (MSME) that are at risk of default. Notably, a large portion of trade receivables is more than 180 days past due and may require loss allowances. This suggests a vulnerability to potential losses if these debts are not recovered. The sources indicate that both trade receivables and loans are largely unsecured, increasing the risk of non-recovery and impacting the company’s financial performance.

Market and Interest Rate Sensitivity: Fino is exposed to market risks, including fluctuations in interest rates and currency exchange rates. The company’s variable-rate borrowings are subject to interest rate changes, which can affect profitability if rates increase. There is sensitivity to an increase and decrease in interest rates. Additionally, exposure to currency risk could affect financial performance if there are significant changes in foreign exchange rates.

While the parent company experienced standalone losses coupled with the high credit risk exposure, the overall financial health of the group is intact. Key indicators such as the net capital turnover ratio and trade receivables turnover ratio show improvements in efficiency and cash flow management. However, Fino PayTech has established a strong presence in India’s fintech sector, leveraging its expansive network and technology-driven services to promote financial inclusion. For continued success, the company will need to effectively manage these risks while capitalizing on the increasing demand for digital financial services.