Care Health Market Trends: Investing in Wellness

The health insurance industry plays a crucial role in ensuring financial security and access to quality healthcare. With rising medical expenses, increasing health awareness, and government-driven initiatives, health insurance has evolved from being a luxury to an absolute necessity for individuals and families across India. As more people recognize the importance of financial preparedness in healthcare, the industry continues to grow at an impressive rate. Care Health Insurance, a key player in this expanding sector, offers a range of health insurance solutions.

The growing importance of health insurance is driven by several key factors, including escalating medical costs, the unpredictability of medical emergencies, and enhanced access to healthcare services. Additionally, government tax incentives allow policyholders to benefit from tax deductions while securing healthcare coverage. These factors are influencing its price trading at [View Current Price of Care Health Unlisted Shares], making it a unique investment opportunity for those looking to tap into India's thriving health insurance market.

Care Health Share Price: Tracking the Future of Healthcare

Care Health Insurance was originally established in 2012 as Religare Health Insurance Company Limited. It was a direct subsidiary of Religare Enterprises, with backing from investors such as Kedaara Capital. The company later rebranded due to a renewed focus on the end consumer. It currently operates on a business model based on the collection of premiums from policyholders, which forms a risk pool. This money is used to cover the medical claims of customers who need it. The company’s success depends on accurately assessing risk and managing claims so that the total amount paid out in claims is lower than the total amount collected in premiums. The company aims to make a profit while ensuring that it can pay out claims when needed.

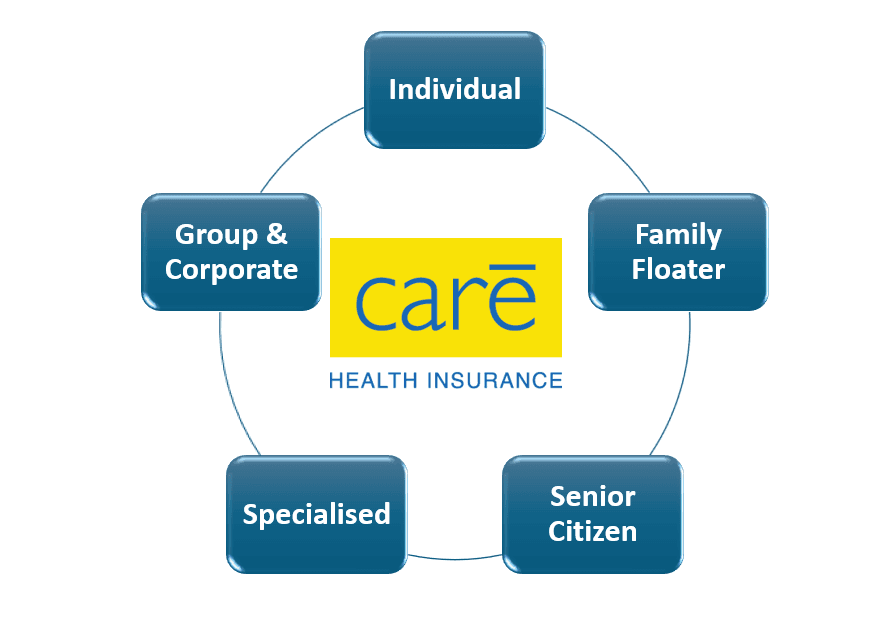

Core Offerings and Product Portfolio

They provide a wide variety of health insurance plans, each tailored to meet different customer needs, from individuals to families and senior citizens. A deeper look into what they offer:

Individual Health Insurance:

This type of plan is designed for a single person. It covers expenses related to hospitalization, such as room rent, ICU charges, doctor’s fees, surgeries, and other medical treatments. Individual health insurance aims to protect the policyholder from large medical bills, making healthcare more affordable when the need arises. This is a great option for someone who does not have family coverage and wants protection for their health.

Family Floater Health Insurance:

Family floater plans are a popular choice because they cover the entire family under one policy. Instead of purchasing individual plans for each family member, this plan pools a single sum insured that all family members can use. For example, if a family has a policy worth ₹10 lakhs, and one member incurs medical costs of ₹4 lakhs, the remaining ₹6 lakhs can be used by another member. This plan offers the flexibility of using the sum insured as per need, making it more affordable and efficient for families with varying healthcare needs.

Senior Citizen Health Insurance:

Health insurance for senior citizens (typically people aged 60 years and above) is specially designed to address the health challenges that come with age. This plan usually provides coverage for hospitalization, critical illnesses, and surgeries, with added benefits like automatic recharge of the sum insured (in case the coverage is exhausted). It also often comes with fewer restrictions, like no mandatory pre-policy health check-ups, making it easier for older individuals to get insured. Senior Citizen Health Insurance is an important safety net for elderly individuals who may need frequent medical care.

Specialized Health Insurance Plans:

Care Health Insurance offers a variety of specialized health insurance plans designed to cater to specific needs. These include Top-Up Health Insurance, which acts as additional coverage to supplement an existing health insurance policy, offering extra protection for major medical events. Personal Accident Insurance provides financial security in case of accidents, covering hospitalization, surgeries, and sometimes even permanent disability or death. Maternity Health Insurance covers the costs of pregnancy, childbirth, and postnatal care for expectant parents. Critical Illness Insurance helps manage the financial burden of long-term treatments for life-threatening diseases like cancer, heart disease, or kidney failure. Additionally, International Travel Insurance covers medical emergencies abroad, offering peace of mind for travelers.

Group and Corporate Health Insurance:

Group Health Insurance: This is a plan provided by employers to their employees as a part of their benefits package. It usually covers basic health needs and may include additional benefits like personal accident cover and wellness programs. Group insurance plans are usually cheaper because the risk is spread across a larger group of people.

Corporate and Micro Insurance Products: Care Health Insurance also offers tailored health insurance solutions for small businesses and organizations, ensuring that employees in these sectors are covered. They also have micro-insurance plans designed for low-income groups, particularly in rural areas, to provide affordable health protection where it is needed most.

Care Health Unlisted Share Price: Unlocking Investment in Healthcare

Being a prominent player in the Indian health insurance sector, it has a proven business model and solid market presence. As a company that’s not yet listed on the stock exchange, the unlisted shares of Care Health present a unique investment opportunity for those looking to tap into India’s expanding health insurance market. Here’s why investing in Care Health Insurance could be a smart move:

Diverse Product Portfolio Driving GrowthCare Health’s wide range of health insurance products—from individual plans to senior citizens, maternity, and critical illness coverage—appeals to various customer segments. With health awareness growing and the demand for health insurance increasing, these diversified offerings position the company well for steady market penetration. As Care Health expands its portfolio, its future growth prospects become more attractive to investors.

Technological Edge and Digital FocusCare Health has embraced technology to improve its operations and customer experience. The company’s digital platforms allow for seamless online policy management, claims filing, and customer support. With a growing number of consumers moving online for their health insurance needs, Care Health's tech-driven approach makes it an appealing investment. Its continued innovation in digital infrastructure will likely lead to enhanced customer engagement, quicker claims settlements, and reduced operational costs, all of which can positively affect Care’s unlisted share price

Government Support and Regulatory AdvantagesWith the Indian government implementing reforms that remove age caps for health insurance and promote the penetration of healthcare coverage, Care Health stands to benefit significantly. The sector's expanding regulatory framework allows for more inclusive products, and Care Health’s alignment with these changes gives it an edge. The company’s ability to adapt to these shifts demonstrates its resilience, making it a reliable option for long-term investment.

Rising Healthcare Costs and Market OpportunityThe escalating costs of medical treatment and private healthcare services in India are creating a growing need for insurance. Care Health, by offering products like top-up insurance and critical illness coverage, is well-positioned to benefit from this trend. Additionally, with India’s low insurance penetration and the vast number of people still uninsured, there is untapped growth potential. This expanding market directly impacts the value of Care Health’s unlisted shares as it captures a larger share of the market.

Strategic Partnerships and Corporate GrowthCare Health Insurance has formed strategic partnerships with corporates, fintechs, and even rural sectors, which helps to expand its reach. Their ability to offer group insurance solutions and micro-insurance products in various sectors further diversifies its revenue streams. As the company continues to collaborate with large entities, its exposure to a wider customer base and increased brand recognition will likely enhance its market valuation.

Peer Standing in the Health Insurance Sector

As of September 2024, Care Health Insurance holds the 4th position in the overall premium collection among health insurers in India due to flexible and personalized policies, leadership in the retail segment due to tailored policies, digitalization, affordable premiums, efficient claim processing, and transparency, which places it ahead of established players like ICICI Lombard and United India Insurance, highlighting its footprint in the health insurance sector.

Discover Care Health Unlisted Shares: Investing in Life and Care

Revenue and Premium Growth

Care Health Insurance has shown growth as in FY 2024, they earned net premiums of ₹5,328 cr., which is a 35.5% increase from the previous year. Additionally, their gross direct premiums (the total premium income before any deductions) grew to ₹6864 crores, showing that Care Health has been successful in expanding its customer base. Higher premiums often mean the company is doing well at securing new customers and increasing its business.

Claims and Expenses Management

Care Health Insurance also had to manage rising claims, as healthcare costs have been increasing. For the year 2024, the net claims incurred (money spent on claims) was ₹3,074 cr., which is more than ₹2,116 cr. in 2023. This increase suggests that more people made claims, possibly due to higher healthcare expenses or more people using their health insurance.

The net incurred claims to net earned premium ratio is 0.58, meaning for every ₹1 the company earned in premiums, it paid out ₹0.58 in claims. This ratio shows how much of the premium income is being used to pay for claims.

Why this matters: A lower ratio (closer to 1) means the company is paying out less in claims compared to what it earns in premiums. In this case, 0.58 is a good number, as the company is retaining more income for other expenses or profits.

Solvency and Liquidity

Care Health Insurance's solvency ratio is 1.74x. This ratio measures how well the company can cover its liabilities (its debts or obligations) with its available assets. The higher the ratio, the more secure the company is in case it needs to pay out large claims.

For context, a solvency ratio of 1x means the company is exactly meeting the minimum requirement set by regulators. Hence, Care Health Insurance has an extra financial cushion, making it a safer bet for policyholders and investors.

Care Health also reported investments of ₹6,632 cr. This means the company holds various assets like government bonds and securities, which it can sell or use to pay for future claims. The larger the investments, the more liquidity the company has to meet claims quickly.

Why this matters: A high solvency ratio and large investments indicate that the company is financially strong and can pay out claims without running into liquidity issues.

Profitability

Despite increased claims and expenses, Care Health Insurance still made a profit after tax of ₹305 cr. for FY 2024. While this is lower than the previous year’s profit of ₹643 cr., it still shows that the company is profitable.

Why this matters: Profitability shows that the company can cover its expenses and still make money. Even though the profit decreased, the fact that the company is still profitable means it is not losing money.

Key Insurance Ratios

- Net Commission Ratio: 0.18xThis ratio tells us how much of the premium income is spent on commissions (payments to agents or brokers). A low ratio means the company isn’t overspending on commissions.

- Expense of Management to Gross Direct Premium Ratio: 0.37xThis ratio shows how much the company spends on management (like administrative and operational costs) compared to its total premium income. At 0.37x, the company spends 37% of its premium income on managing the business, which is a reasonable amount and indicates good cost control.

- Combined Ratio: 0.95xThis ratio combines both the claims paid out and the company’s expenses to show how profitable the company is overall. A ratio below 1 is good because it means the company is earning more than it is spending on claims and expenses.